The six fundamental flaws underpinning the energy transition

Zoe Hilton , Aidan Morrison , Alex Bainton , Michael Wu

May 2, 2024 · AP67

Executive summary

The Australian Government wants to transition our electricity system to net zero carbon emissions by relying on wind and solar power – excluding alternatives such as small nuclear reactors. Its justification for this switch rests on the claim that a renewables-dominated system is environmentally beneficial and economically superior to using fossil fuels and nuclear energy.

But its premise is based on a flawed argument which has left out key elements which portray a different picture.

Energy Minister Chris Bowen, policymakers and other public figures use the CSIRO’s GenCost report and the Australian Energy Market Operator’s (AEMO) Integrated System Plan (ISP) to support their argument. These reports defend a belief of economic superiority for renewable energy which relies on two distinct claims:

That renewable energy is cheaper than alternatives, including fossil fuels, regardless of any cost of carbon or other policy constraints; and

That the planned transition is the cheapest pathway to reach Australia’s emission reduction targets.

The first claim is principally supported by GenCost, and the second by the ISP, though these claims are frequently conflated in policy discussions. However, the Centre for Independent Studies (CIS) has identified many critical flaws in the analysis of both reports that destroy any credible support they could give to these claims.

CIS research has found that using coal-fired generation for the majority of baseload demand, which Australia is dismantling, would be significantly cheaper in the near term than relying on intermittent renewables for 90% or more of energy generated, as the ISP and GenCost do. CIS has also found that GenCost overstates the cost of nuclear plants because it does not consider cost-effective and established models.

Second, CIS found the ISP has been undermined in its aim to develop the lowest-cost system by finding the optimal combination of infrastructure across states. State and Federal governments ‘declare’ projects to be required, without a comprehensive system-wide business case. The ISP then treats these projects as ‘sunk’ and forces the system to optimise around them, increasing costs. If the most inexpensive system was built — even relying almost entirely on renewables — it would likely look markedly different to the system being built. In particular, it would exclude very deep, pumped-hydro storage (e.g. Snowy 2.0) and the rapid advancement of high-voltage, interstate transmission which is underway.

This paper focuses on the question of how Australians have been led to believe two false claims: that renewables are the cheapest and that the cheapest version of a renewables-dominated system is to be built.

To answer this question, CIS has categorised the flaws in GenCost and the ISP under six headings. These flaws are misleading about the true costs of the proposed energy transition.

The six fundamental flaws of GenCost and the ISP are:

1 – Out-scoping costs

GenCost excludes storage and transmission costs incurred before 2030, making wind and solar appear cheaper than coal, gas and nuclear, even with high wind and solar penetration;

The ISP relies on rooftop solar and home batteries to provide generation and storage but excludes their costs from the model;

The ISP excludes the cost of recycling wind turbines, solar panels and batteries, making renewables appear cheaper than they are over their lifetime.

2 – Out-scoping carbon

The ISP excludes emissions from the manufacture of wind, solar and batteries making them seem cleaner. This restriction of ‘Scope 1’ emissions means the ISP will increasingly export emissions to China, whilst creating the appearance of meeting net zero ambitions locally.

3 – ‘Match-fixing’ the energy transition

The ISP claims a renewables-dominated grid is the cheapest option for Australia’s energy system without comparing any alternative, effectively fixing the outcome from the beginning, as the only baseline scenario without a binding renewable energy or carbon target has been removed;

The ISP manipulated the selection of inputs to force a faster timeline for transmission projects.

4 – Overfitting the model

The ISP has an overfit model that assumes favourable weather decades in advance and builds flexible gas capacity to compensate for years predicted to have poor weather for renewables. In reality, the grid will have to be prepared for almost any weather, every year, requiring greater investment to ensure reliability.

5 – Disintegrating the integrated system

The ISP method for determining the value of individual projects does not treat the energy system as an integrated whole (i.e. a system of smaller sub-systems) but rather a collection of parts largely independent of one another, allowing uneconomic projects to be approved and costs passed onto consumers;

The ISP treats government-committed projects with costs yet to be finalised as determined and does not assess their benefits making transmission projects that link these assets seem more valuable.

6 – Cherry-picking data

GenCost cherry-picks a single, overestimated data point from a cancelled project to use as the cost estimate for Small Modular Reactors (SMR) and does not include any data from large-scale, nuclear plants — making nuclear energy seem more expensive;

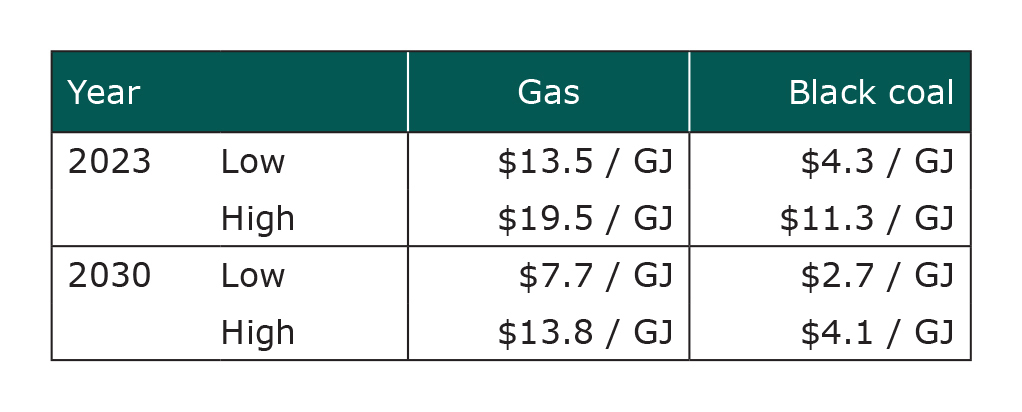

GenCost cherry-picks coal and gas price estimates so that fuel price spikes induced by the Ukraine war are locked in for the lifetime of new coal and gas plants;

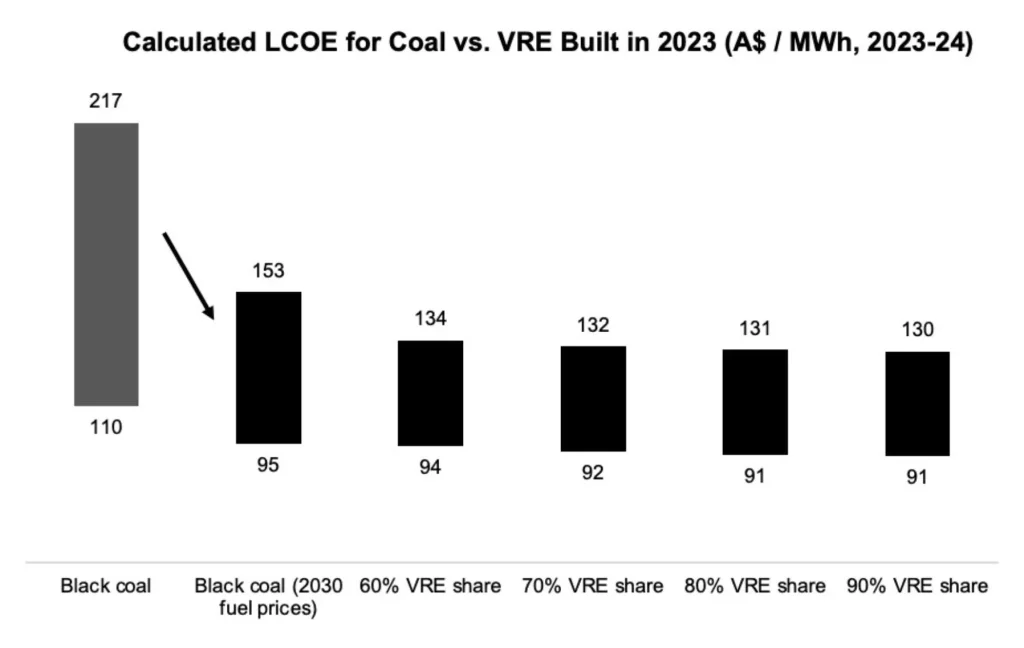

GenCost uses unrealistic assumptions about construction costs for new coal plants, reinforcing the illusion they are more expensive than renewables;

The ISP chooses certain future years in which transmission projects show greater cost benefits, then justifies projects going ahead as soon as possible in an entirely different year;

The ISP selects years in its reliability analysis in which no reliability breaches occur and ignores years when a breach is likely to occur.

Introduction

Weather-dependent renewables have been consistently promoted by the Albanese government as the only option for Australians to have cheap, reliable and clean energy. Any attempts to question this or suggest an alternative technology have been denounced as climate denialism,[1] fossil fuel lobbying[2] or culture-war distraction.[3] This has affected the public policy debate around the relative costs and benefits of renewable energy.

This paper contends the declining quality of the energy debate can be traced to a growing rift between what policymakers and public figures claim the evidence supports and what the evidence actually supports.

On the first question of the energy trilemma — whether an energy system dominated by wind and solar is more environmentally friendly or ‘clean’ — there are clear grounds for debate. When only carbon emissions are considered, there is compelling evidence that wind and solar have significantly lower emissions per unit of electricity produced than coal.

But the environmental argument should also consider other factors, such as preserving the local natural environment. Land-intensive energy sources (e.g. wind and solar) will perform worse in this regard than technologies with a smaller footprint (e.g. coal and nuclear).

The second part of the trilemma is reliability. This is possible for a wind and solar-dominated grid, but not without great cost. Adding additional systems (e.g. extra transmission) sufficient to ensure reliability may also have an environmental impact.

The third part of the energy trilemma is cost. Energy Minister Chris Bowen[4] and other public figures[5] have claimed a renewables-dominated energy system — even including the costs of the transmission, storage and firming generation required to make it reliable — is still cheaper than the current coal-dominated system.

This claim, which is the foundation of current policy and has benefited from substantial affirmation in the media, appears to hold broad support from a large body of evidence. However, on close inspection, CIS has found there is essentially no credible evidence to support this claim.

Mr Bowen[6] and other public figures[7] tend to base their claim that renewables are not only clean but also cheap and reliable on two crucial sources: CSIRO’s annual GenCost report[8] and the Australian Energy Market Operator’s (AEMO) biennial Integrated System Plan (ISP).[9]

The purpose of GenCost is to provide updated cost estimates for investors in new-build electricity generation, storage and hydrogen production.[10] It is also used to provide forward-projected capital costs as an input to the ISP and claims to show that renewables are the cheapest, new-energy technology to build.[11]

The ISP provides a whole-of-system plan for the National Electricity Market,[12] aiming to design the lowest cost, secure and reliable energy system capable of meeting emissions targets.[13] It claims the lowest cost path for Australia’s energy transition is an energy system dominated by renewables and backed up by transmission, storage and gas.[14]

The outcomes of these reports are frequently conflated,[15] but careful reading exposes two distinct claims for which each are used as evidence:

GenCost: That renewable energy is cheaper than alternatives, including fossil fuels, regardless of any cost of carbon or other policy constraints.

Integrated System Plan: That the planned transition is the cheapest pathway to reach Australia’s emission reduction targets.

The key distinction between the two is that the ISP’s claim of economic superiority is confined to act within the boundaries of existing carbon budgets and renewables targets. However, GenCost is used to support the stronger claim that the renewables system is cheaper overall. In doing so, it relies to a significant extent on some of the more comprehensive modelling undertaken for the ISP’s integration of generation with transmission and storage. Indeed, GenCost is a collaboration between AEMO and CSIRO and a significant part of the funding for GenCost comes from AEMO.[16] Consequently, the merits and flaws of the reports are intertwined.

The net effect is that these reports have succeeded in creating a general aura of economic superiority for renewable energy over any alternative — including both the fossil-fuelled status quo or nuclear — with the overarching suggestion that our most respected technical and scientific institutions agree about this.

This report contends that neither GenCost nor the ISP credibly supports the two specific claims they each purport to make and the contention that renewables are clearly cheapest is not just unsupported but untrue.

This paper outlines six fatal flaws of logic that have allowed two major public institutions to continually repeat an incorrect statement. There are many other lesser problems with both reports which are not addressed in detail here.

The six flaws are not minor and are contradictory to the objective, evidence-based analysis that should underpin policy. Everyone, of all political persuasions — including ardent supporters of renewable energy, fossil fuels or nuclear energy — should be concerned with ensuring each of these is resolved.

Each of these six flaws is independently capable of collapsing the integrity of one or more of the formal claims of GenCost and the ISP. Taken together, they show that the overarching claim about the economic superiority of renewables in Australia’s energy transition plan is incorrect.

Flaw #1: Out-scoping costs

Sunk costs before 2030 in GenCost

CSIRO’s GenCost report outscopes storage and transmission project costs incurred before 2030, effectively treating them as a sunk cost,[17] which makes variable renewables (i.e. wind and solar) seem far cheaper than coal, gas and nuclear, even at high levels of penetration.[18]

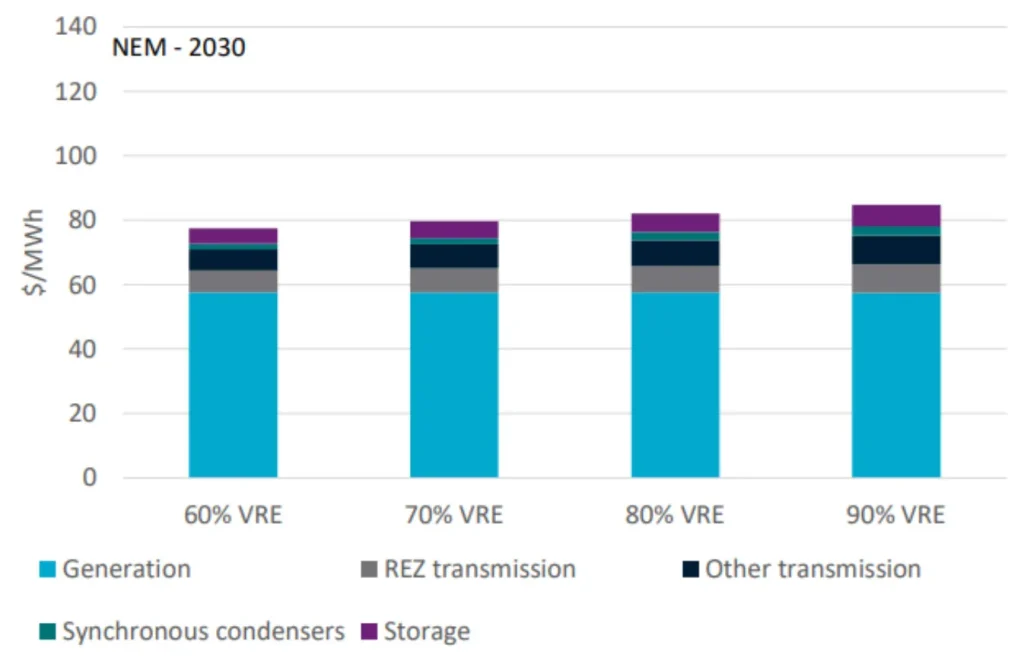

GenCost is primarily concerned with costs to investors for different new-build generation and storage technologies at a particular time, not whole-of-system costs.[19] The key data GenCost uses to compare these technologies are capital costs and the Levelised Cost of Electricity (LCOE) — the average price of electricity an investor would need to receive over the life of their investment to recover both capital and operating costs.[20] However, the 2030 LCOE analysis treats pre-2030 transmission and storage projects as

‘free’,[21] making variable renewables appear to have relatively low integration costs compared to the costs of generation (see Figure 1).[22]

Figure 1. Levelised costs of achieving 60%, 70%, 80% and 90% annual variable renewable energy shares in the National Electricity Market NEM in 2030.

As renewables usage increases, the GenCost model forcibly retires coal plants.[23] This should result in transmission and storage costs dramatically increasing with higher usage, as reduced reliable baseload power necessitates renewable energy being transported further and stored for longer.[24] Although this sharp increase is commonly found in other studies estimating costs for increasing renewables penetration,[25] GenCost counter-intuitively depicts a negligible increase in integration costs from 60 to 90% variable renewables (Figure 1). If the costs of pre-2030 transmission and storage projects were fully included, the increase would likely have been much greater.

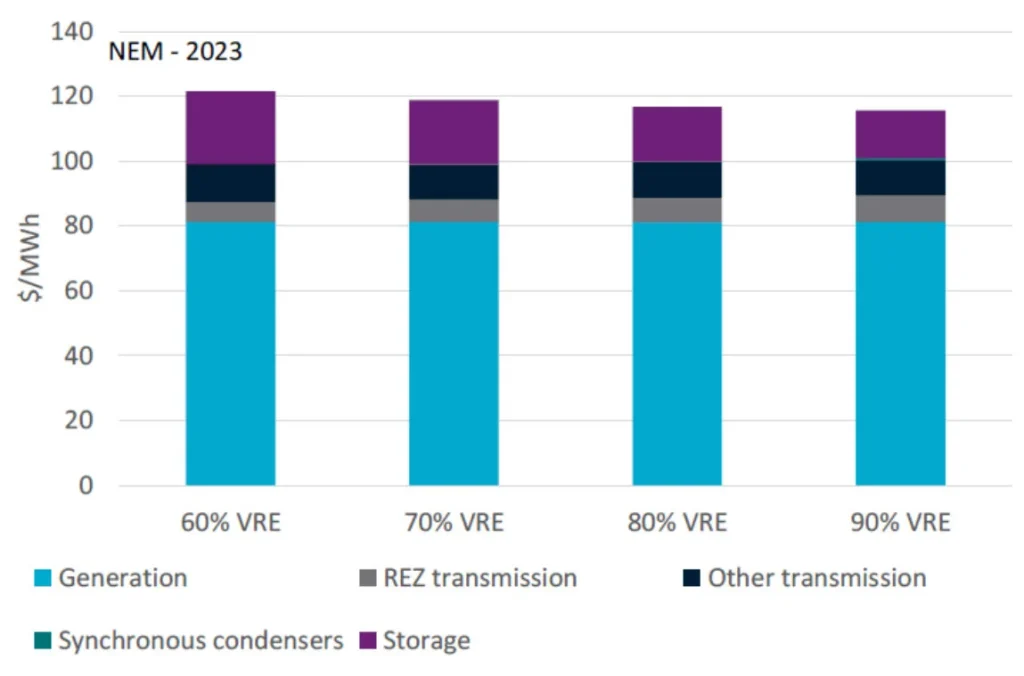

In response to concerns about the exclusion of pre-2030 integration costs being raised by stakeholders during previous GenCost report consultations, CSIRO has attempted to estimate these costs in the Draft 2023-24 report.[26] These 2023 integration costs include two gas plants, Snowy Hydro 2.0 and other major storage projects[27] and 11 transmission projects flagged by AEMO’s Integrated System Plan as being needed by 2030.[28] CSIRO “abstracts from reality” and assumes these projects can be completed immediately so that they can be included in the 2023 LCOE, [29] without accelerating the depreciation of these assets.[30] This means the 2023 analysis has essentially assumed the costs of pre-2030 transmission and storage projects can be fully paid off in 7 years so that they are completely free for the 2030 analysis, without any additional costs arising from this compressed timeline. This does not reflect reality, neither showing only the costs to investors nor the full costs a consumer would realistically face.

Additionally, no attempt was made to calculate what proportion of integration costs arising from these projects is necessary at each share of variable renewables — instead all costs are included regardless of renewables share.[31] This results in the pattern of decreasing costs with increasing penetration of renewables (Figure 2), because the cost of the pre-2030 storage and transmission projects can be spread over more variable renewable energy generation the greater the variable renewables share.[32] In reality, fewer transmission and storage projects would be needed with lower usage of renewables. Rather than clarifying the integration costs of renewables, this analysis only serves to mislead readers into thinking integration costs will become cheaper as more renewables are added to the system.

Figure 2. Levelised costs of achieving 60%, 70%, 80% and 90% annual variable renewable energy shares in the NEM in 2023.[33]

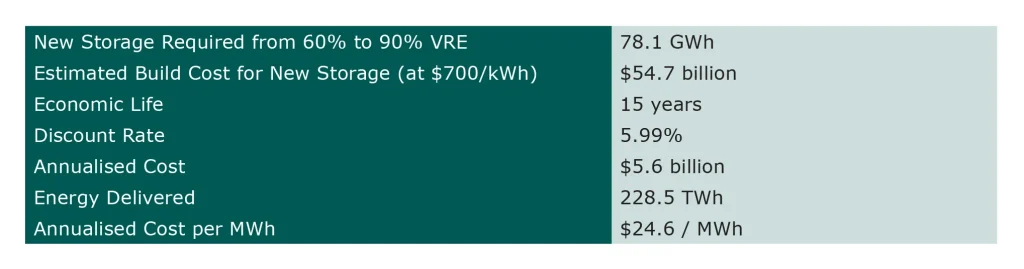

When compared with projections from the ISP, which CSIRO considers a “benchmark”,[34] the 90% variable renewable integration costs for 2023 seem unreasonably low. Analysing data from the ISP shows that the ratio of the cost of storage per unit generation is at least 75% greater for 90% variable renewables compared to 60% variable renewables.[35] Furthermore, calculating the annualised costs of batteries suggests a cost of approximately $24.60 per MWh (see Table 1), far more than the roughly $17 per MWh suggested in Figure 2, which should also include costs for Snowy 2.0 and other pumped hydro projects. These checks provide further evidence that the GenCost estimates for variable renewable integration costs are too low and are aberrant in their lack of any dramatic increase with variable renewable share, which is a common feature of other related studies.

Table 1. Calculation of the annualised cost of additional storage capacity from 60% to 90% VRE.

CSIRO could have simply presented the costs an investor would face for different generation technologies and denied the Energy Minister’s claims that GenCost proves renewables are better for consumer’s energy bills than fossil fuels.[36] Instead, CSIRO has continued to support the unjustified claims of the Minister by attempting to quantify pre-2030 integration costs that no investor would face (i.e. transmission costs paid for through consumer bills). Although well-intentioned, this attempt has resulted in a confused analysis ultimately divorced from reality.

For future reports, CSIRO should either:

Commit to conducting a complete assessment of total system costs, as would be faced by consumers (or taxpayers), at varying levels of renewables penetration, or

Limit the analysis to only costs faced by an investor (i.e. excluding transmission costs) and clarify that GenCost does not provide evidence for a renewables-dominated system being cheaper for consumers.

Consumer Energy Resources treated as free in ISP

The ISP relies heavily on rooftop solar and home batteries, known as Consumer Energy Resources (CER), to provide generation and storage in coming decades, but does not include these assets as a cost.

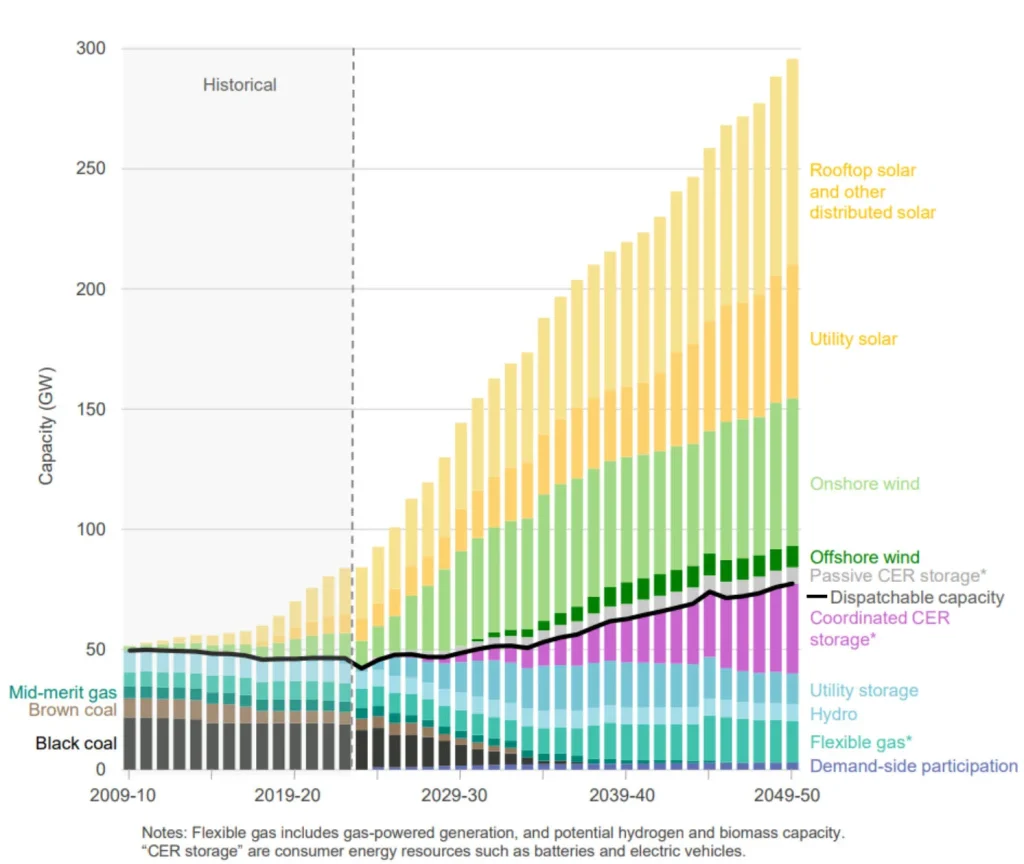

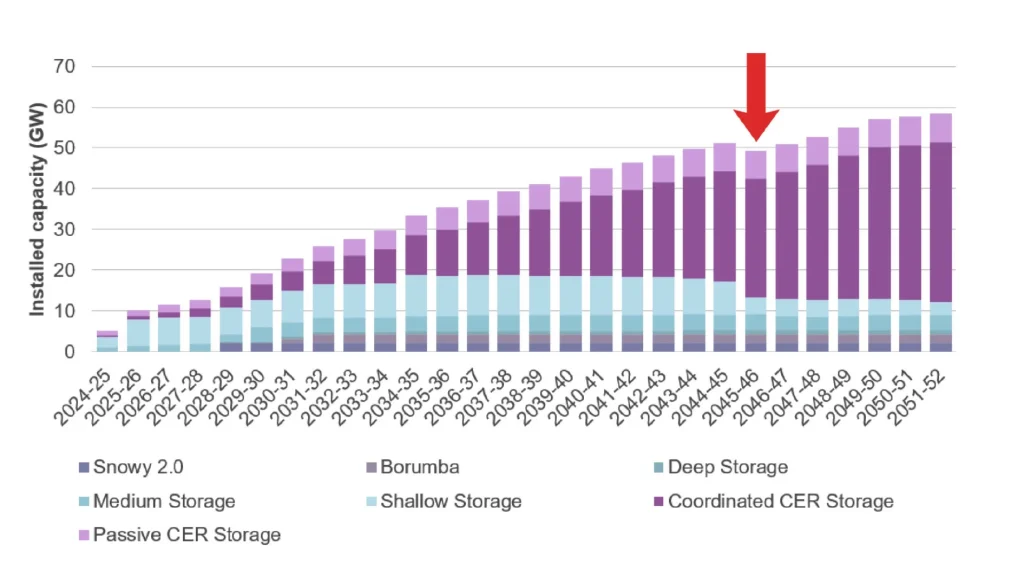

Rooftop solar makes up the majority of solar capacity in the grid for the ISP’s forward projections (Figure 3). Likewise, coordinated CER storage (i.e. home and EV batteries connected to Virtual Power Plants [VPPs] that control their charge and discharge to the grid) makes up the lion’s share of storage from the mid-2040s onwards (Figure 3). Yet despite the forecast preponderance of CER, AEMO has “not included costs for household or residential batteries and solar PV because those are decisions that households and businesses make on their own” – the solar panels and batteries paid for by consumers are instead taken as an “input”.[37]

This crucial assumption is glossed over in the ISP’s executive summary, which states that the benefits of the Optimal Development Path include avoiding “$17 billion in additional costs to consumers”, without any mention that the annualised capital cost of all generation, storage, firming and transmission infrastructure, estimated at $121 billion,[38] does not include the cost of CER.[39]

Figure 3. NEM capacity projections in GW in Draft 2024 ISP Step Change scenario from 2009-10 to 2049-50.

These excluded costs are significant, with the total cost of rooftop solar and consumer batteries up to 2050 totalling around $360 billion at today’s prices using GenCost’s estimates.[41] This is much higher than the $130 billion cost of large-scale solar and batteries up to 2050 (which the ISP does include).[42]

AEMO has responded to stakeholder concerns about the treatment of CER as a static input by stating that the ISP “doesn’t try to dictate what consumers do” but rather adapts to consumer preferences.[43] However, these preferences are largely shaped by government policy that determines the financial benefit consumers expect when making those investments. When determining the forecast uptake of rooftop solar in the ISP model, AEMO takes into account government policies that provide financial incentives for consumers (e.g. Small Technology Certificates and feed-in tariffs)[44] — without including them as a system cost. AEMO also includes financial incentives for CER storage (i.e. home batteries and EVs) to forecast uptake,[45] including South Australia’s $3000 subsidy for new EVs,[46] which ended in January 2024.[47] Furthermore, AEMO makes the assertion that the “optimistic outlook for coordinated CER storage” will require “continual reforms of tariffs, market incentives and policies”[48] — without any attempts to estimate the associated costs.

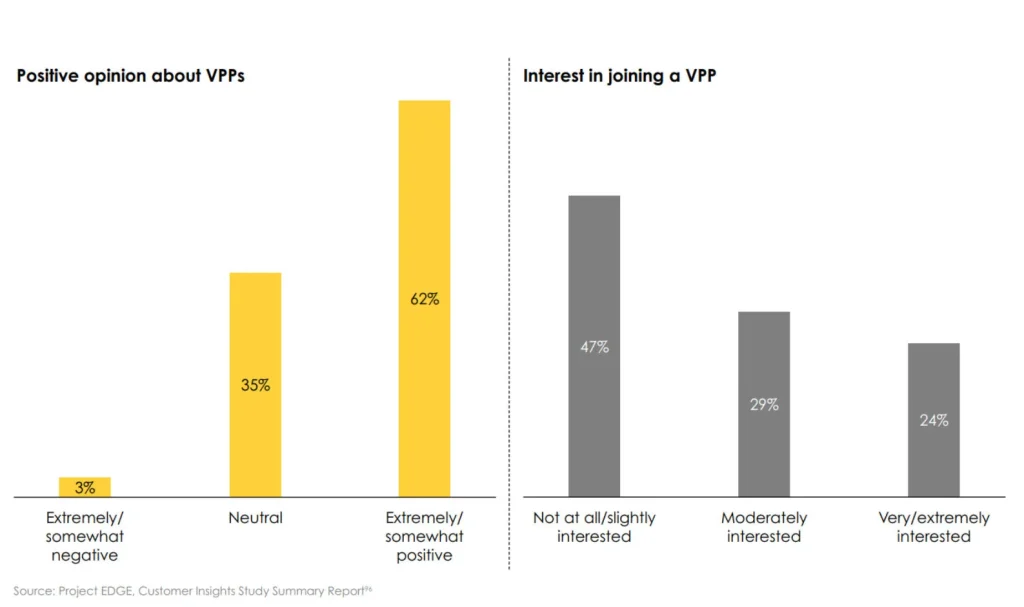

Financial incentives are clearly needed to convince consumers to allow their batteries to be coordinated. The coordinated CER trial Project EDGE found that almost half of consumers had little to no interest in joining a VPP (Figure 4). The project report further stated that the widespread adoption of CER and VPP to reduce carbon emissions was “less valued by consumers relative to having a reliable supply of power, saving money and receiving good service.”[49]

Thus, not only do consumers want to be adequately compensated, they also want to use their battery to maintain a reliable source of power (including during peak demand or a blackout). This is at odds with the way VPPs operate, as they are incentivised to sell power from customer’s batteries back to the grid when spot prices are highest, which will occur during a period of peak demand or blackout. The contradictory incentives for CER customers and VPPs therefore make achieving the projected levels of coordinated CER storage difficult — and expensive.

Figure 4. Consumer perceptions about VPPs and interest in joining a VPP from Project EDGE surveys.

Financial incentives are also needed to encourage consumers to change EV charging behaviour. The ISP models convenience charging (i.e. charging at home immediately upon arrival after work during peak time) as dropping from around 73% of the time in 2022-23 to below 36% in 2050, while coordinated charging (i.e. charging during non-peak times and discharging to the grid during peak times) rises from 0% to around 32%.[51] There is no opportunity cost modelled with this forecast — instead, the ISP references the “right incentives and systems” that will encourage EV owners to relinquish control of their EV batteries and charging habits to serve the needs of the grid.[52] Research reveals less than 17% of EV owners would consider changing their charging time to between 10am and 2pm (i.e. when solar output is at its peak) without an incentive.[53]

Significant outlays will be required to upgrade distribution networks to ensure grid stability as CER installations grow. The cost of distribution network upgrades is significant, with an Energeia project paper estimating the total cost of mitigating over-voltage due to solar installations over the next 20 years as being between $0.7 to $1.1 billion, depending on the level of CER adoption.[54] Yet, the ISP does not take these costs into account.[55] Flagging this issue, the ISP Consumer Panel stated: “While AEMO describe the ISP as a ‘whole of system’ plan, it is in practice, a ‘whole of transmission’ plan with limited involvement of distribution networks.”[56]

AEMO’s mischaracterisation of what is essentially a transmission planning exercise as a ‘whole-of-system’ plan contributes to policymakers such as Energy Minister Chris Bowen inappropriately using the ISP as evidence that a renewables-dominated grid is cheap.[57] The Minister said the ISP “looked at… in current dollars, the total cost out to 2050 of the entire generation, storage and transmission and came up at $121 billion.”[58] As this number excludes the $360 billion of CER calculated above and the associated costs of distribution network upgrades, the true cost would be greater than the figure quoted by Mr Bowen.

Policymakers need to be able to directly compare different mixes of technologies in the energy system to have accurate information about whole-of-system costs, as government incentives and programs greatly influence consumer and investor decisions. By excluding the costs associated with CER (such as capital, installation, maintenance, incentives to encourage uptake and behavioural shifts in charging and distribution network upgrades), AEMO has not provided a fair comparison of the costs and benefits of CER versus large-scale solar farms and batteries. This lack of co-optimisation prevents policymakers from making informed decisions and prevents consumers from knowing the true cost of their decisions regarding rooftop solar and home batteries as well as the ensuing bill impact of the energy transition.

According to the CSIRO, large-scale solar and batteries are cheaper than small-scale rooftop solar and home batteries,[59] which means the ISP’s heavy reliance on uncosted CER is likely to increase overall system costs for consumers. Additionally, network service provider Ausgrid has stated their “marginal expenditure typically occurs on low voltage distributors”, the part of the network most affected by rapidly growing CER.[60] This raises the question of whether distribution network upgrades required by CER growth will drive up system costs far more than the transmission network upgrades needed by an equivalent amount of large-scale solar and batteries. Despite growth in CER likely to increase total system costs, AEMO continues to use CER to offset the amount of large-scale battery storage[61] and solar (Figure 3) in the grid.

To provide policymakers and consumers with a whole-of-system plan for the energy transition, AEMO should model CER as a system cost, including capital, installation, maintenance and incentives to encourage uptake and behavioural shifts in charging and distribution network upgrades. CER should be co-optimised to accurately compare the costs of a low-CER grid versus a high-CER grid.

Costs of recycling renewables and battery waste not included in ISP

Costs associated with recycling wind turbines, solar panels and batteries are not included in the ISP, making renewables seem cheaper than they are over their lifetime.

AEMO’s claim to include disposal and recycling costs of generation assets in their model[62] is false. Retirement costs for solar and on-shore wind are taken from a 2018 GHD report that does not include disposal or recycling of solar panels and wind turbines.[63] Further, all large-scale battery retirement costs are excluded because “disposal cost data is not known.”[64] AEMO also does not attempt to include any retirement costs for offshore wind facilities, claiming their long construction time means that “retirement costs would be incurred beyond the end of the ISP modelling horizon.”[65] This reasoning is flawed, as no investor would start such a project without having a cost estimate for decommissioning and rehabilitating the site once the plant reaches the end of its life.

The omission of disposal and recycling costs essentially means the ISP has assumed all waste from solar panels, wind turbines and large-scale batteries is either abandoned on-site or taken to landfill at no cost. This is unrealistic, given Australia’s legislative environment is increasingly making recycling the only option. In Victoria and South Australia, solar panels and batteries have been banned from entering landfill and must be recycled or stored until they can be recycled.[66] Western Australia has announced similar restrictions, Queensland is in the consultation phase and the federal government is also developing a mandatory product stewardship scheme which could make solar panel manufacturers and importers liable for recycling costs.[67]

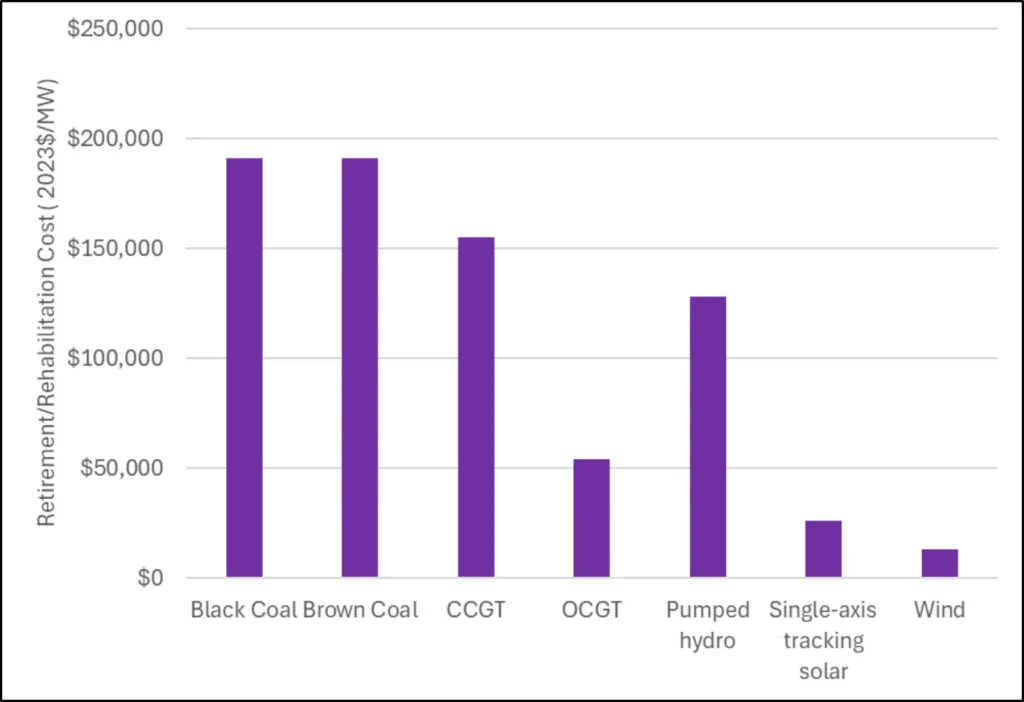

None of these costs is included in the Draft 2024 ISP. The ISP’s retirement/rehabilitation cost estimates for wind and solar therefore appear low compared to coal, gas and pumped hydro (see Figure 5).

AEMO should include the estimated costs of disposal and recycling for all wind turbines, solar panels and batteries, including CER, in their model so the ISP can accurately optimise system costs arising from generation and storage.

Figure 5. Retirement/rehabilitation cost estimates of different generation technologies in the Draft 2024 ISP.

Flaw #2: Outscoping carbon

Lifecycle emissions of renewables not considered in ISP

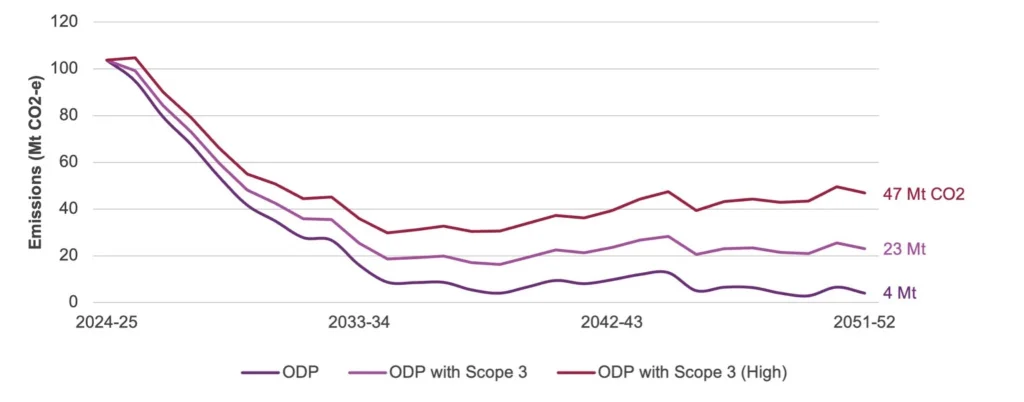

The ISP does not include emissions arising from the manufacturing of wind, solar and battery systems, making renewables seem cleaner than they are. It also means the claim that this plan allows us to comply with a particular carbon budget is not credible in the global sense, since significant emissions will simply be exported to other countries whose emissions will increase.

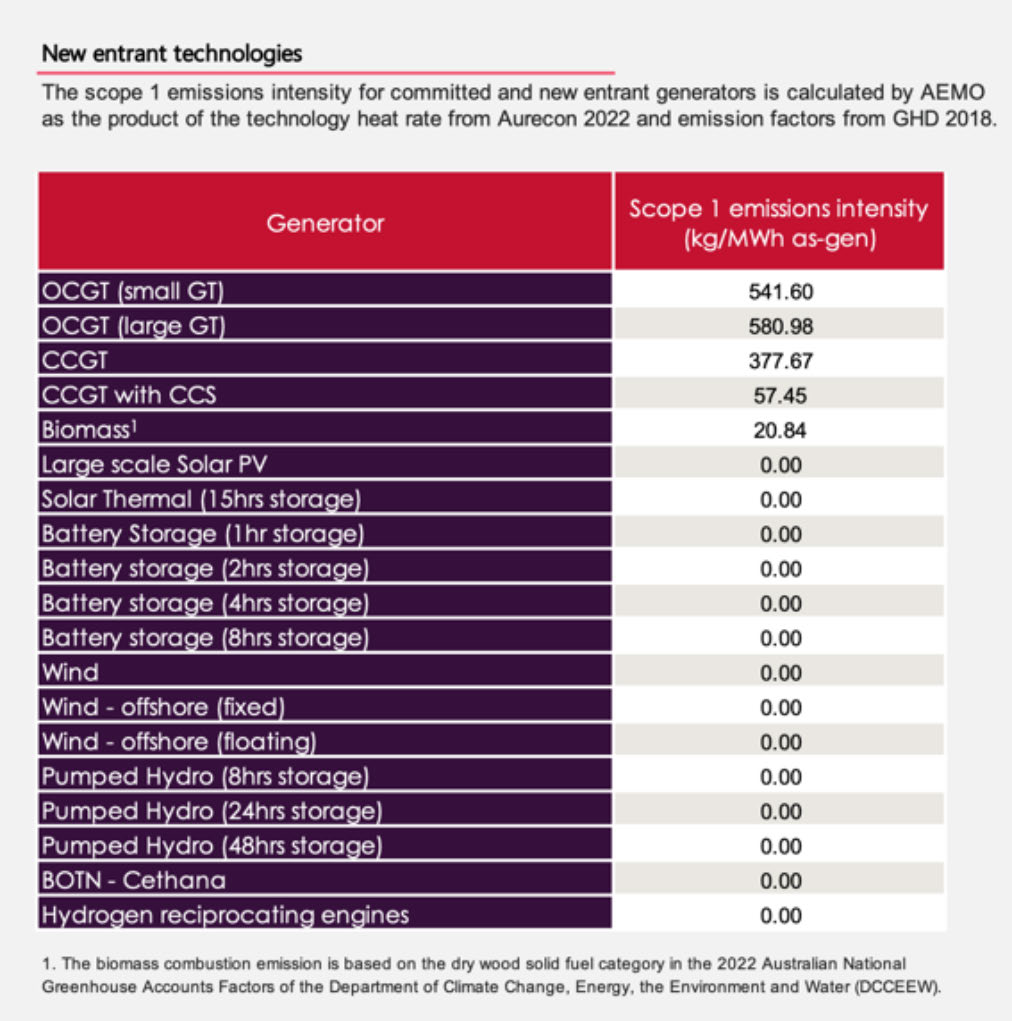

The ISP accounts only for direct emissions (i.e. Scope 1), such as the burning of coal or gas, and excludes the emissions arising from production of the steel, concrete, composites, silicon and electronics that comprise wind, solar and battery systems.[69] This results in the model assuming solar, batteries and wind are entirely emissions-free (Table 2). This exclusion of indirect (i.e. Scope 3) emissions in the ISP’s accounting effectively exports large quantities of emissions to the countries which manufacture solar panels, wind turbines and batteries for Australian customers. For example, China is Australia’s main supplier of solar panels[70] and a key supplier of wind turbines[71] and battery storage systems,[72] with an electricity grid highly reliant on coal, particularly for energy-intensive applications such as manufacturing.[73]

Table 2. Emissions intensity for new entrant technologies in the 2023 Inputs, Assumptions and Scenarios Report (IASR).

Scope 3 emissions, including the emissions generated from the manufacturing process,[75] often account for more than 70 percent of a business’ carbon footprint, as noted by Deloitte.[76] These indirect emissions are the only source of greenhouse gas emissions associated with solar panels, wind turbines and battery systems. By excluding lifecycle emissions of generation and storage technologies and only considering direct (Scope 1) emissions, the ISP likely over-represents the emissions reductions that would occur with high usage of solar, wind and batteries. Figure 6 shows emissions intensity in the Optimal Development Path in the Draft 2024 ISP has the potential to be around 6 times higher than AEMO has forecast, if reasonable estimates of Scope 3 emissions are included from solar, wind and batteries. Using the top end of Scope 3 estimates, emissions intensity could be 12 times higher. This raises doubt over whether the current energy transition plan will achieve net zero by 2050. Note: The ODP emissions trajectory is taken from the Draft 2024 ISP ODP’s projected emissions intensity under Step Change.

Figure 6. Projected emissions intensity in the ISP’s Optimal Development Path, with CIS’s central and high estimates of emissions intensity if lifecycle emissions for solar, wind, and batteries are included.

For the ISP’s emissions intensity projections to accurately capture the differences between fossil fuels and wind, solar and batteries, AEMO needs to include modelling of Scope 3 emissions in accordance with the carbon intensity of the grid where generation and storage technologies have been or are likely to be manufactured. This will prevent Australia going down a path where our domestic emissions are reduced at the expense of increasing emissions in the country selling us solar panels, wind turbines and batteries.

Flaw #3: ‘Match-fixing’ the energy transition

Lack of a neutral baseline scenario in the ISP

The ISP claims a renewables-dominated grid is the cheapest option for our energy system without a comparison to any alternative, namely coal or nuclear. This failure to compare technologies on an even playing field amounts to apparent ‘match-fixing’ the energy transition. AEMO does this by excluding any scenario without renewables and carbon targets that could be used as a neutral baseline and reveal the true cost of policy decisions.

The CEO’s preface for the ISP states: “Renewable energy connected by transmission, firmed with storage and backed up by gas is the lowest cost way to supply electricity to homes and businesses through Australia’s energy transition.”[85] This is a tautology — there is no other conclusion the ISP could have reached regarding the cheapest option, given its exclusion of nuclear due to its legal status and the removal of the only baseline scenario that could have allowed for coal refurbishments or replacements in the model.

If AEMO had framed the ISP’s purpose as being restricted to identifying the cheapest path for building transmission to support a renewables-dominated grid, this exclusion of coal and nuclear would be understandable. But instead, the ISP has made the broader claim of finding the “lowest cost way to supply electricity”. This has resulted in Energy Minister Chris Bowen and Science Minister Ed Husic announcing the ISP “confirms that a renewable grid with hydro, batteries, flexible gas and transmission is the lowest cost way to deliver a secure and reliable energy grid.”[86] This assertion implies that other feasible alternatives have been tested through a cost-benefit analysis when none has.

Rather, AEMO has allowed government policy (i.e. renewables and emissions reduction targets and a dismissal of nuclear) to dictate the assumptions in its model, thus ‘match-fixing’ the outcome. This circularity — where policy shapes the ISP which then endorses the policy — limits a transparent evaluation of alternatives, entrenching predetermined policy directions without a full accounting of their costs and benefits.

Feasible alternatives to renewables were excluded from the analysis through the selection of scenarios that enforces binding renewable energy and carbon targets.

In the 2021 Inputs Assumptions Scenarios Consultation (IASC), there are five scenarios — Slow Change, Steady Progress, Progressive Change, Step Change and Hydrogen Superpower — all of which assume a 26-28% reduction in emissions by 2030.[87] However, only the latter three scenarios assume a target of net zero by at least 2050 — Slow Change and Steady Progress do not have this constraint.[88]

The Steady Progress scenario was originally derived from the Central scenario in the 2020 ISP,[89] previously named ‘Current Trajectory’,[90] and was consequently considered a highly relevant reference point. The other scenario derived from ‘Central’ was initially called ‘Net Zero 2050’[91] before being renamed ‘Progressive Change’.[92] This scenario was very similar to Steady Progress, except for a much larger industrial electricity load and a binding emissions reduction target.[93] Steady Progress was the most realistic counterfactual to assess potential costs of transitioning to renewables, due to its lack of a binding carbon budget and use of “central estimates for technological and macroeconomic influences” — particularly coal prices.

At the original Delphi Panel[94] for the 2022 ISP, Steady Progress was given the same weighting of likelihood as Hydrogen Superpower, an ambitious scenario assuming Australia becomes a major exporter of green hydrogen.[95] This meant that participants rated a scenario with no binding emissions reduction target as equally likely as an extremely optimistic scenario with “significant technological breakthroughs and social change to support low and zero emissions technologies”.[96] Together with Slow Change, the Delphi Panel gave an 18% weighting to scenarios that did not include the binding net zero target.[97] Slow Change assumed slower-than-anticipated emissions reduction, depicting a future in which Australia did not reach the economy-wide decarbonisation objectives of the Emissions Reduction Plan.[98]

However, after the announcement of the 2050 Net Zero target at COP26, AEMO discarded the results of the first panel, calling on a new panel to develop new weights for the 2022 ISP.[99] There was no public consultation on the results of the second panel — even the official ISP Consumer Panel members were excluded — before these weights were adopted by AEMO as the Draft ISP weights.[100] Also, the size and composition of the panel was in breach of the official ISP Methodology.[101]

For the Second Delphi Panel, Steady Progress was removed from consideration, apparently due to its “failure to meet net zero ambitions”.[102] However, no explanation was given for retaining Slow Change, which also did not have a binding net zero target. Given that Slow Change had far fewer votes in the first Delphi Panel (5% instead of 13%),[103] removing the least likely scenario that wouldn’t meet the target would appear to be logical.

Given that no coal plant refurbishments or new brown coal were allowed by AEMO’s assumptions,[104] only new or refurbished gas plants or new black coal would be possible. However, by removing Steady Progress with its central price assumptions, the only scenario able to show how much coal and gas the cost-optimising model would recommend without a binding carbon target (i.e. Slow Change) used coal and gas price assumptions higher than any other scenario.[105]

This may have been a critical factor in determining the eventual generation mix. Including Slow Change, and excluding Steady Progress, meant AEMO could present relatively uniform scenarios in the 2022 ISP that all eventually reached net zero without replacing coal or gas with only a 4% weighting given to the Slow Change scenario with no binding emissions reduction target.[106]

The AEMO decision to re-run the Delphi Panel, without oversight from the Consumer Panel or public consultation, removed the only scenario that could have been used as an appropriate counterfactual in the 2022 ISP.

This issue of a lack of neutral baselines becomes more problematic in the 2024 ISP, with AEMO removing Slow Change, the only scenario remaining without a binding renewable energy or carbon target.

The removal of Slow Change means all remaining scenarios model a 43% emissions reduction target in the carbon budget up to 2030, an 82% share of renewable generation by 2030 and a net zero emissions target by 2050.[107] Though hamstrung by high coal and gas prices, Slow Change represented the last opportunity to establish a baseline to test the benefits of a proposed infrastructure pathway when emissions targets are missed and renewables penetration is lower.[108]

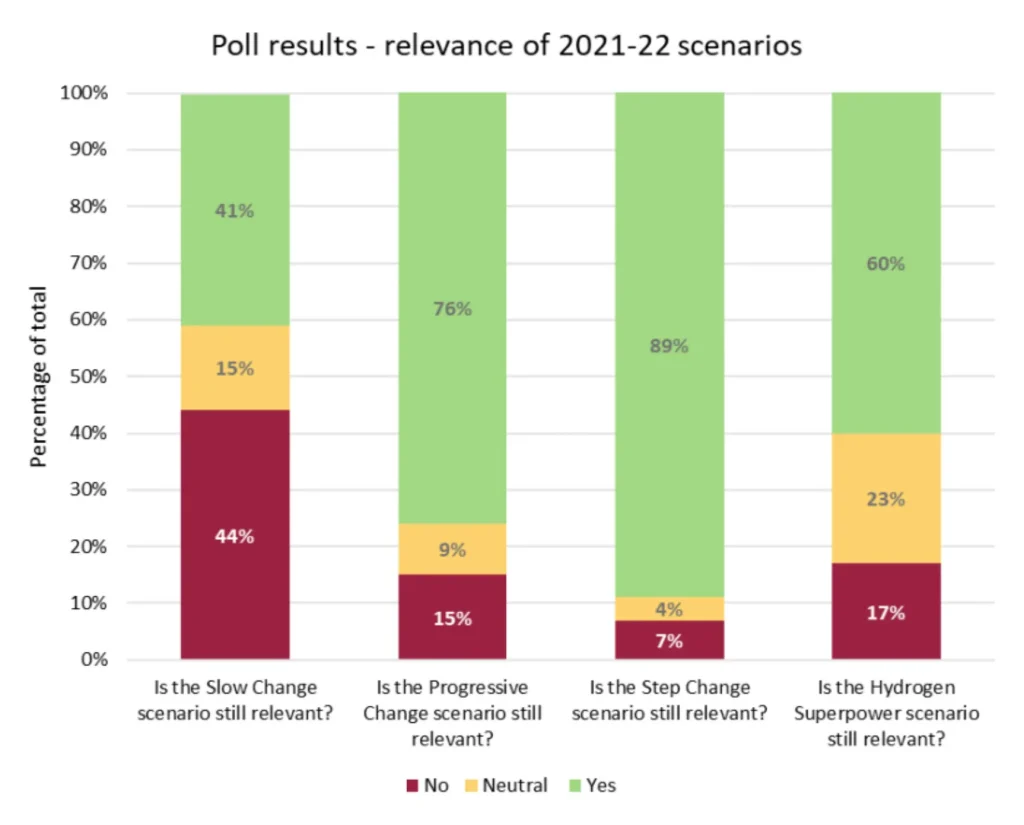

AEMO decided to remove Slow Change on the basis it was “no longer consistent with the pace of transformation required by the collection of policies facing Australia’s energy industry”.[109] AEMO further justified this decision by claiming “a majority of stakeholders supported the Slow Change scenario’s removal, consistent with its very low relative likelihood in the 2022 ISP”.[110] This is false.

A majority of stakeholders did not support the removal of Slow Change with 56% either agreeing that the scenario is still relevant or not having an opinion either way (Figure 7). In fact, the majority of comments from stakeholders in the consultation webinar were supportive of keeping Slow Change in the analysis, particularly as a “bookend”, “benchmark”, “baseline” or “counterfactual” which is “necessary to check for regretted investment”.[111]

Figure 7. Poll results from 2023 Preliminary Scenarios Webinar feedback regarding the relevance of scenarios in the 2022 ISP to the Draft 2024 ISP.

As one stakeholder pointed out: “It’s likely to be worthwhile including one scenario that is relatively ‘pessimistic’ in terms of abatement progress, economic growth, tech costs etc in order to get a wide spread of possible scenarios. Scenario planning is not just about what stakeholders want to happen.”[113]

Another stakeholder emphasised the increasingly volatile geopolitical environment as being a reason for keeping Slow Change: “The scenario may still be relevant for representing the uncertainty in economic recovery post pandemic and into the Russian invasion of Ukraine. It represents a de-prioritisation of decarbonisation and more emphasis on energy security.”[114] Even some of those who thought the scenario unlikely supported it remaining with one stakeholder saying: “It may not be a likely scenario but it is important to have a good spread to see the impact of different futures. It also avoids the concern of ‘bias’.”[115]

AEMO did not heed the concerns of these stakeholders and proceeded to remove Slow Change, thus creating a bias towards the high end of emissions reduction and renewables capacity trajectories in the scenarios tested in the ISP model . As AEMO has also not performed sensitivity testing for emissions reductions or renewables capacity falling below government targets, the cost to the consumer arising from over-investment in transmission if targets are missed remains unknown.

AEMO needs clarity about the ISP’s purpose and findings, particularly the fact that it does not test the full range of feasible alternatives for Australia’s grid and therefore cannot support the claim that a renewables-dominated grid is the cheapest way of supplying electricity. To test this claim, the AEMO must include an unconstrained counterfactual scenario in its analysis that does not presuppose policy commitments in order to reveal the true cost of government targets and commitments. Without it, the selection of scenarios towards more ambitious targets prevents a proper cost-benefit analysis being performed on an even playing field.

Forcing preferred transmission outcomes through input and constraint manipulation

The second Delphi Panel discussed previously saw votes flow from the (eliminated) Steady Progress to Step Change and saw the Progressive Change scenario (renamed from the previously most popular Net Zero 2050 scenario) fall to second place, also losing votes to Step Change.[116] This substantially increased the overall weightings of scenarios that required the most rapid and ambitious uptake of renewables and assumed the fastest closures of coal.

This shifted the optimal timings of three of the largest transmission projects that were previously listed as actionable: VNI West, HumeLink and Marinus Link. If the initial weightings of the first Delphi Panel were used, with Progressive Change the most likely scenario and Steady Progress equally weighted with Hydrogen Superpower, none of these projects would have been advanced immediately as actionable projects.[117]

Given that multiple billions of dollars of investment hinge on this shifting of scenario weights, considerable attention should be paid to the circumstances in which the initial weights were discarded and the panel re-run. With the Net Zero 2050 scenario already being the initial winner and Slow Change having only a small portion of the votes,[118] it would have been perfectly reasonable to use the initial weightings. No serious claim can be made that the possibility of Australia adopting a net zero 2050 target was not appropriately considered in the initial weightings.

The overall effect of re-running the Delphi Panel was not just to eliminate the most likely counterfactual without a carbon target but also to ensure regulatory approval of many billions of dollars of transmission at the fastest possible schedule. Without any credible claim that the initial Delphi Panel was worse than the second one, this amounts to AEMO seemingly intervening to shift the path of the nation’s transition plan away from what is optimal for consumers to a plan that better suits the interests of transmission companies and renewable energy investors.

Flaw #4: Overfitting the model

Model builds just-in-time gas capacity for perfectly-predicted weather in ISP

Overfit models work very well for a limited set of data but tend to fall apart when faced with the unpredictability of the real world. AEMO has overfit the ISP’s model by assuming perfect weather for the next few decades and building flexible gas capacity before weather events which are poor for renewables, while also timing battery retirements so they occur just after such years of unsuitable weather.

AEMO does not test the ISP model against a range of potential weather conditions to ensure grid reliability. Instead: “AEMO’s energy market modelling is optimised with the benefit of perfect foresight of VRE [i.e. wind and solar] output and operational demand within each simulated day.”[119] This foresight of perfect weather decades in advance is a serious departure from reality. AEMO then ensures unserved energy (i.e. blackouts) are avoided by “allowing the model to build flexible gas to take into account those chances of unserved energy”.[120] Flexible gas capacity projections are thus overfit to a particular set of weather conditions.

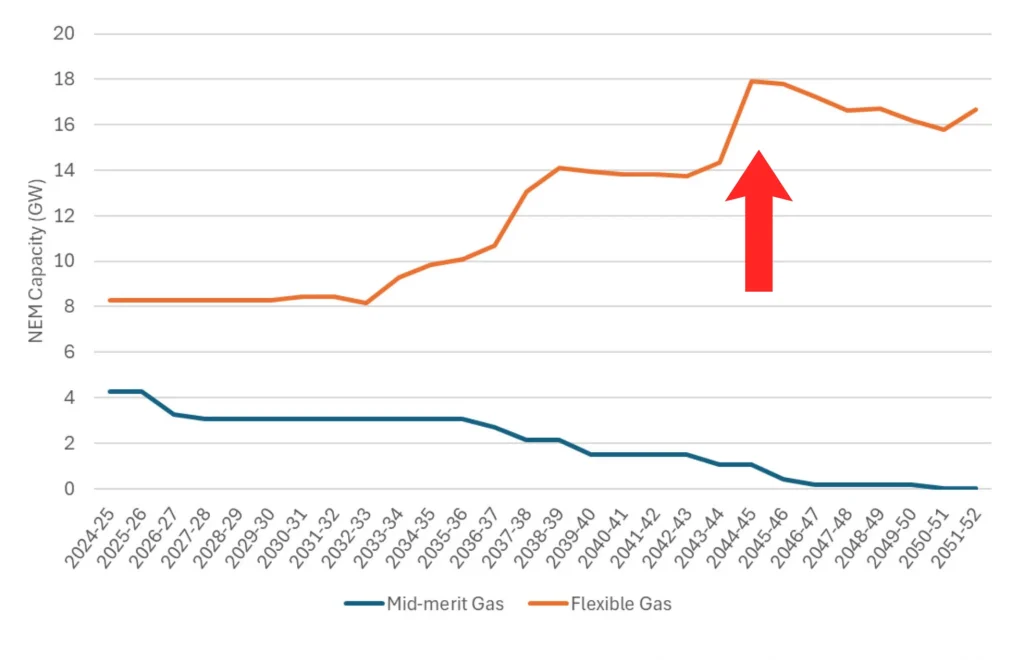

This results in the pattern of flexible gas capacity for the next few decades being very lumpy, with some years having no new capacity built or reduced capacity from retirements, while other years have unprecedented amounts of new capacity built (Figure

. The biggest increase in one year occurs in 2045, when 4 GW of new capacity is built, reaching a peak in total capacity of 18 GW. To understand the scale of building 4 GW of flexible gas in one year, the largest power station in Australia (Eraring) has less than 3 GW of capacity.[121]

Figure 8. Gas capacity for mid-merit gas and flexible gas across the NEM in the Draft 2024 ISP ODP under Step Change.

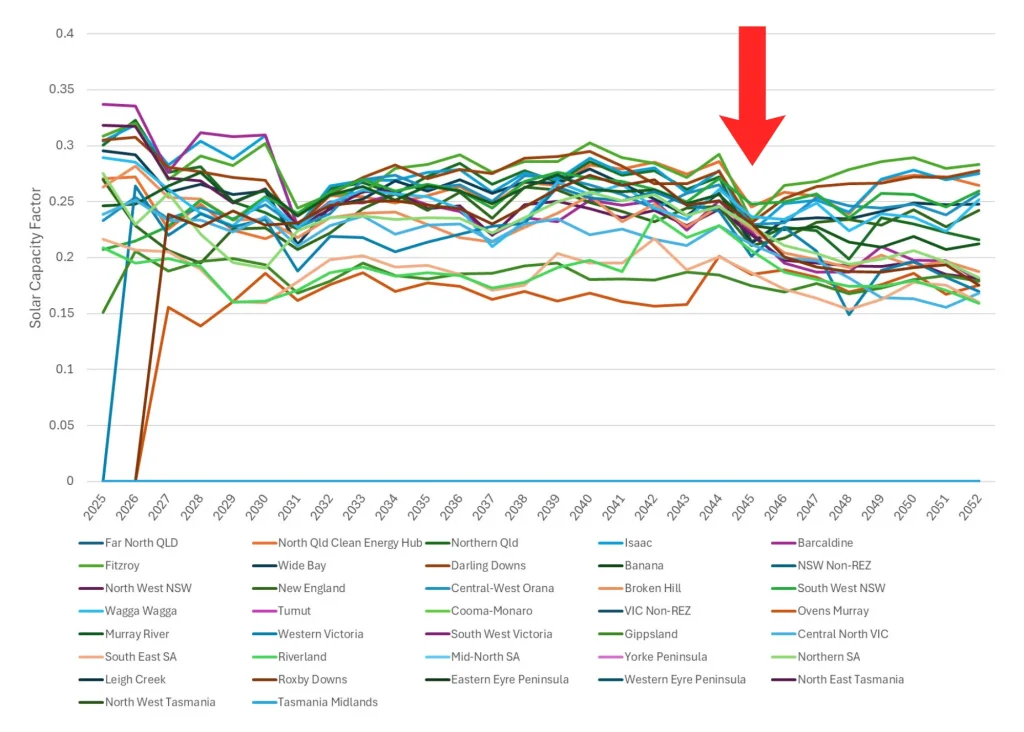

2045, the year of peak flexible gas, is conveniently the same year in which solar capacity factors across most solar farms experience a marked drop (Figure 9). The ISP model builds just-in-time gas capacity to get through this apparently cloudy future year with no consideration of what would happen if the bad solar year came one or two years earlier when gas capacity is lower.

Figure 9. Solar capacity factors for solar farms across the NEM in the Draft 2024 ISP ODP under Step Change.

The ISP model also perfectly times large-scale battery construction and retirement so that extra storage capacity is available for apparently cloudy future years. The storage capacity forecast in the ISP grows steadily, apart from a curious dip in 2045-46 (Figure 10). This occurs because shallow storage capacity (1-2 hour batteries) is assumed to halve in one year, falling from 8 GW in 2044-45 to 4 GW in 2045-46. This represents the retirement of the 4 GW of shallow batteries built in 2025-26, as they have an assumed economic life of 20 years.[124] The retirement of these batteries falls directly after 2045, the year assumed to have particularly low solar output, so they can be used to support the grid through the solar drought and then never replaced again.

This means AEMO has, as in the case of flexible gas, overfit the construction of large amounts of batteries in the ISP model by assuming a bad solar year will occur in 2045. The model choosing to build such a large amount of batteries in one year instead of spreading construction to avoid sudden decreases in capacity is further evidence that the ISP’s model is not fit for purpose and is likely to fail when faced with the unpredictability of weather events.

Figure 10. Draft 2024 ISP forecast for NEM storage capacity in GW by year under Step Change.

AEMO should fix the overfitting of the ISP model by running it through a range of potential weather sequences. This could be done by testing the capacity in each year of the model to ensure no major blackouts will occur if 1-in-30-year lows in solar and wind output were to eventuate. Without doing this, consumers have no assurance the energy transition plan laid out by AEMO will prevent major blackouts in bad weather years.

Flaw #5: Disintegrating the integrated system

Methodology breaks apart integrated system in ISP

AEMO’s method for determining the value of individual projects does not treat the energy system as an integrated whole but rather a collection of parts largely independent of one another. This allows uneconomic projects to be approved and costs passed onto consumers.

AEMO uses the take-one-out-at-a-time (TOOT) method to provide an estimate of the sensitivity of each transmission project in the Optimal Development Path to cost variations. This is supposed to determine each project’s benefits and the threshold of cost increases that would lead to a project no longer being beneficial for the grid.[126]

TOOT analysis is performed by taking out a particular transmission project and any associated capacity augmentations from the Optimal Development Path (e.g. removing the transmission link that deepens the connection capacity between a Renewable Energy Zone and the rest of the grid, as well as removing the increased renewables capacity that would be built in that zone).[127] The TOOT results are crucial for the ISP to ensure final approval is not granted for previously recommended transmission projects that face cost blowouts which would make them uneconomical.

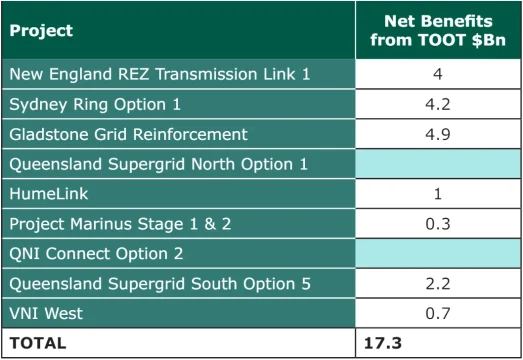

However, the TOOT analysis in the ISP is unsuitable to serve its intended purpose. This is made clear by the fact that the sum of the calculated net benefits of just a subset of transmission projects in the Optimal Development Path matches the total net benefits of all transmission projects. AEMO claims the total net benefits of the Optimal Development Path amount to $17 billion[128] — but according to the TOOT analysis, this $17 billion sum is exceeded by adding up the individual project benefits even before Queensland Supergrid North or QNI Connect have been added (Table 3). This means individual projects have been valued as greater than logically possible given the total value of the system, thus artificially inflating their actual benefits to make them appear more desirable.

This issue has arisen because the TOOT analysis breaks down the integrated system into independent parts, many of which do not make sense to build unless complementary parts are also included. To illustrate, it is as though AEMO determined the value of a bicycle by taking away each individual part and seeing how much less the bicycle was worth as a result. If the chain is removed, the bicycle is almost worthless and so the chain is assigned almost the same value as the whole bike. Likewise for the pedals, the wheels and so on until the sum of all the individually-valued parts is many times that of what the bicycle is actually worth.

A better approach would be for AEMO to consider certain projects that are dependent on one another for their value as subsystems that should not be separated in a TOOT analysis. This approach ensures a proper understanding of the threshold of transmission cost increases that would make a project no longer viable.

Table 3. Net benefits of projects in Draft 2024 ISP, excluding Qld Supergrid North, QNI Connect and minor projects that were not provided.

Government-committed projects locked in without proper scrutiny in ISP

The ISP treats government-committed projects with costs yet to be sunk as locked in and therefore makes no attempt to assess their benefits to the system. This, combined with the way the system is dismantled by the TOOT analysis, results in transmission projects that link these assets appearing more valuable than they would be otherwise, paving the way for further projects to be locked in without the whole system ever being fully optimised.

Transmission projects that have not passed the required cost-benefit test, the Regulatory Investment Test for Transmission (RIT-T), can now be considered locked in by going through a less rigorous state government process that does not optimise the whole system. For example, the NSW Government’s new Transmission Efficiency Test allows transmission projects to bypass the more stringent RIT-T[130] and proceed by simply proving the project can be delivered efficiently, regardless of whether it is a good idea in the first place.[131] This sidestepping of the RIT-T has occurred with the Central-West Orana REZ Transmission Link.[132] Similarly, an amendment to the National Electricity (Victoria) Act 2005 allows the RIT-T to be bypassed at the Victorian Energy Minister’s discretion.[133] Passing off responsibility for verifying the economic viability of a project to the states in this way essentially allows boondoggles to be built as long as they are built efficiently.

Committed projects being treated as sunk costs have inflated the value of the major transmission projects linking NSW and Victoria: HumeLink and VNI West. Snowy Hydro 2.0 have been treated as sunk costs in the ISP model because it is a federal government commitment expected in 2028,[134] despite, after a series of significant delays, only $5 billion of funds has been spent, with $7 billion yet to be spent.[135] Even if just $6 billion of Snowy 2.0’s costs were included in the model, the net present value of HumeLink without competition benefits would sink from $43 million to negative $4.9 billion,[136] meaning that consumers would seem to be better off if planning for HumeLink and construction for Snowy 2.0 ceased immediately.

Likewise, the Central West Orana Renewable Energy Zone (REZ) Transmission Link and the Western Renewables Link are considered locked in by the ISP model since they have been granted regulatory approval, pushing up the value of HumeLink and VNI West.[137] The Western Renewables Link has undergone the RIT-T[138] but without VNI West, it would not have been worth building since it needs VNI West to connect Melbourne to the grid.[139] The interdependent nature of these projects means treating one as a sunk cost will inflate the value of the other, making it impossible to determine whether building both is cost-effective. Worse is the treatment of the Central West Orana REZ Link as a sunk cost, given it has not undergone the RIT-T[140] and is crucial for connecting the REZ to HumeLink and VNI West, inflating its value further.[141]

Also there is the temptation to expand the capacity of a declared project as much as possible to inflate the value of the transmission links connecting it to the broader grid, since any added capacity will be incorporated into the model at no extra cost. This has already occurred for the Central West Orana REZ Link with the original 3 GW capacity being doubled to 6 GW.

The treatment of committed projects as sunk costs, especially those that have not gone through a rigorous cost-benefit analysis, means the ISP has been prevented from examining an alternative scenario where a whole set of projects (e.g. Snowy Hydro 2.0, HumeLink, and VNI West) are found to be uneconomic and do not proceed. In this scenario, states could have developed their own renewable energy zones, storage and gas firming with less interconnection, saving billions on transmission projects that could then be invested in other parts of the system.

AEMO should not treat projects as locked in with costs sunk simply because a government has committed to them when those projects have not had the full cost-benefit analysis as part of the whole system. All projects for which significant unspent funds remain should be treated as parts of the integrated system that can be added or taken away to find the Optimal Development Path. Without this occurring, governments won’t have accurate information on the relative value of their declared projects to the system and consumers won’t be able to have confidence in the Optimal Development Path serving their long-term interests.